My birthday was a few weeks ago and cliché, yes, but it’s crazy to believe a whole year has flown by again. I’ve left the country for the first time, became a CFP, and traveled and ate my way through a few new states.

And now, with three banks failing at the same time and possibly a fourth on its way, I can never seem to get a handle on time.

But with birthdays come annual texts, random calls of good wishes, and sometimes great gifts.

She knew I wouldn’t spend the money on myself, so my best friend got me the exact shoes she knew I wanted. And now, I have this $100 gift card that I know I want to spend on something, but I need to figure out what to spend it on. (Just to give you an idea of my life’s problems.)

Still, it makes me wonder when spending money on myself became such a chore.

When I was 17, $100 would be gone in 8 seconds. I wouldn’t think about saving it for a rainy day. I wouldn’t think about how to MaXimIZe iTs uTiLity.

I’d try to stimulate the economy right then and there.

Speaking of money and birthday gifts, opening and funding an UTMA can be a great gift for your kids, grandkids, or even nieces and nephews. Instead of toys and clothes they’ll quickly grow out of, why not use that money for something that could provide them with value today and tomorrow. With the median starter home price at nearly a half million dollars, this gift could grow over the years to make life a little bit easier as they enter adulthood.

UTMAs are set up by parents, grandparents, or aunts and uncles who mean well and just want to see the next generation do well in life. Not to mention, they’re much easier and cheaper to set up than establishing a trust fund.

But, unlike a bank account, it doesn’t allow the child to tap into it as they choose. Instead, it’s a minor’s trust account managed by a parent/guardian who decides if/how this money is invested.

However, what happens when they turn 18 (or 21 in some states) is something to be wary of.

Many parents may need to realize this account can also be a double-edged sword. Once they become the age of majority, all assets in the UTMA become theirs to use as they see fit.

As I look back on it, at that age, I wonder if $50,000, or even $200,000 would have changed my short-sighted perception.

Would the same motivations still be there? What about all the good I could do with that money? The family members I know could use some extra cash. Once I bought everything I thought I wanted, would that have changed what fate had already laid out for me?

This could greatly influence any young adult who has yet to even crest their early twenties. The question is, how do you ensure your kids would maintain financial responsibility if plenty of cash was suddenly in their possession?

The Baby Bonds Act

While this might all sound gravy, there’s an interesting bill working its way through the senate that speaks to the other side of the coin.

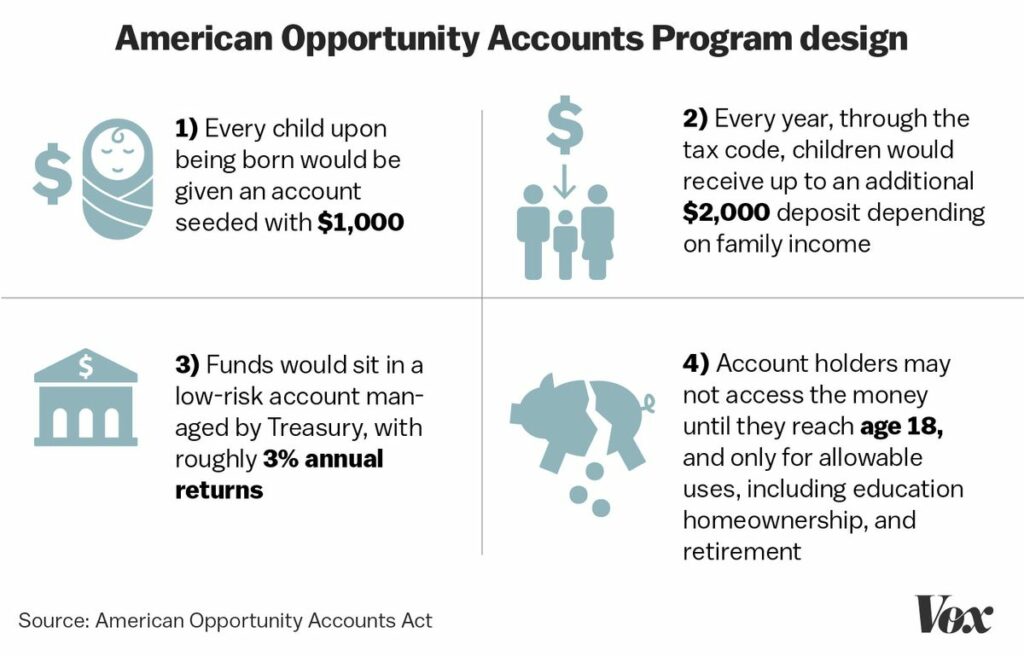

Senator Cory Booker (NJ) and Representative Ayanna Pressley recently reintroduced the American Opportunity Accounts Act, which they wittingly dubbed the “Baby Bonds Act.”

The idea stems from A Birthright to Capital, the research on children’s savings programs economists Darrick Hamilton and William Darity Jr published in 2020.

Albeit very left-leaning, I thought this was interesting and timely. If passed, the bill would set aside $1,000 for every U.S. child and deposit up to $2,000 per year depending on where the family’s income falls from the federal poverty line. It’s disproportionately aimed at benefiting children who come from extremely low-income households.

There’s no argument that too many families (especially families of color) have been severely left behind in this game to obtain wealth. And when you’re coming from neighborhoods and backgrounds like this, social mobility is merely a pipedream. Or, your name becomes a legend amongst a select few.

These funds set aside could help begin to bridge the enormous wealth gap between the haves, the have-nots, and the probably-never-wills.

Now, there are strict guardrails around the use of these funds. Unlike an UTMA, upon turning 18, the children can only use the funds for education, homeownership, entrepreneurship, or retirement expenses after age 59. So, essentially, these bonds have financial responsibility measures built into them.

How to Prepare Them

Going back to UTMAs, I don’t often see balances well into the six-figure range for these accounts.

Especially given that money can be rather tight for young couples and since you can only deposit up to the annual gifting limit ($17,000 for 2023) per year without any funky tax consequences. Yet, the largest UTMA balance I’ve ever seen was well over $2,000,000!

But it’s important to note that if you’re looking to save for a specific reason, like their education, for example, there may be better tools available.

Again, even with the best intentions, when a large swath of cash hits their bank account, say two million dollars, they could be off to the races. Honestly, what would you do?

Once this money is in their hands, they have no forced financial responsibility on how they’ll choose to spend it.

It’s worth it’s weight in gold to introduce them to what’s going into this account and why as early as you can.

If they’re too young for jobs, give them opportunities to ‘earn’ money helping around the house, or even the neighborhood. Get them involved in the decision-making over how the money is handled over time, then help them understand their future spending options. I think once they get to see their money grow and experience the feeling of seeing it waver will help curb their enthusiasm to blow it on cheap thrills; depleting its future potential.

Trust me, a brand new blacked-out Jeep Wrangler at 18 is much more seductive than thinking about how to MaXimIZe mY MonEy’S uTiLity.

You know your child better than anyone. So if you believe extra precautions should be taken, think twice about the balance you may like the UTMA to reach before they become ‘legal.’

If you want to know some creative ways on what to do once they turn 18 and the money is theirs, you’ll have to reach out to me and find out.

A Great Birthday Gift

Of course, there is a large discrepancy in lifestyles between those with the discretionary income to fund a UTMA and those targeted by the Baby Bonds Act. However, in either case, you should lead by example. Children are little sponges who pick up more things than you may care to admit. Making wise, conscious decisions with your own financial decisions will, in turn, help create their money story. Which could be for the better.

I spent so much of my adolescent years just wishing we had more money. Thinking, surely, that would fix all of our problems.

Well, one day, I got exactly what I wished for. I moved out of my Aunt’s house west of Atlanta and in with my little sister and her parents in Ohio. And they were, in fact, in a much better spot financially than where I was coming from. Problem solved, right?

Well, my naïve wishes cost me what little I did have. I lost many of my early high-school relationships that were just beginning to bud. I lost touch with my older brother for a long time. And what I didn’t know then was that that would be the last day I would ever see my grandmother.

“If man could have half his wishes, he would double his troubles.” If only I were wise enough to understand what Benjamin Franklin meant back then.

You’ve heard countless stories of how money doesn’t buy happiness. We get that. However, what it does buy are options. Options to open many closed doors. But, as I’m learning, that’s nothing compared to where hard work and a good reputation can take you.

Throwing some money in an UTMA is a great birthday gift for a little one. Don’t get me wrong. I’m sure a new toy could easily erase all of the world’s injustices to a 6 year old. But know, that money today could pay for future birthday gifts, music or dance lessons, or become a big help down the road. Investing that money instead could pay off in the long run and make things a bit easier for them when they’re all grown up.

I forget where I’ve heard this before, but just be remember that with great power comes great responsibility.