The Road to the Trillion Dollar Wealth Transfer Isn’t Paved with Gold

Hey guys. I hope you all had a great Thanksgiving and were able to stuff yourself silly as I did.

Last week was my cheat week, so now I have to spend the rest of the year working it off.

Does anyone else have family or a significant other who puts up the Christmas decorations immediately after Halloween or Thanksgiving? The older I get, the more I realize Thanksgiving gets treated like some second-rate holiday. It barely has a chance to be a holiday before it gets replaced by Big Christmas.

Anyway, I wanted to catch you up on a long-overdue story.

Back in September, Future Proof 2025 was another amazing year, with friends, music, and thought-leaders worth traveling across the country to see. The first Future Proof in 2022 was not only my first time in LA, but my first time in California. Since then, I’ve made it a point to try something new and/or explore different attractions in SoCal.

Looking back at these pictures only makes me miss the summer even more.

Anyway, coming from the East Coast, where your Uber driver is most likely silent and on the phone at the same time, I guess I’m always a little jaded by the chatty bunch I typically get in Cali.

This year, as I’m on my way to the airport, my Uber driver—let’s call him Mark—and I are trading stories about this and that, eventually getting around to what we do on the outside.

If I’m remembering correctly, he owns an audio installation and repair business specializing in high-performance cars. Audis, BMWs, Porsches. And high-end trucks like your Raptors and Rams. As he explains, it’s a premium service, but his customers are high rollers and car enthusiasts who have no problem spending thousands of dollars to upgrade their stereo systems.

But what really stuck out were two things he shared with me.

First, his business partner recently passed away (Complete strangers share these kinds of things with me all the time. Don’t ask me why).

They had an informal agreement that his partner would buy him out, and Mark would retire soon.

Well, that’s not happening anymore.

But he also shared with me that, although he has employees—each playing a specific role on the labor side of the business—none are really equipped to be business owners. At least not yet.

Instead, he would like his son to take over the business. His son… who is 28… and couldn’t care less about his dad’s business.

I can’t confirm that it’s all true. Maybe he was looking to guilt-trip this out-of-towner into leaving a bigger tip. Perhaps. But let’s assume he was telling the truth.

Regardless, it’s all very fascinating and a microcosm of major forces at play here.

The great wealth transfer is well underway, and as a member of my firm’s trust and estate planning team, I have seen a mix of good intentions, some really creative planning, some non-existent planning, and realities many families would rather not talk about until it’s too late. But don’t get seduced by the eye-popping numbers.

The $84 trillion-dollar (or whatever it’s up to now) wealth transfer isn’t going to be as beautiful and majestic as the headlines make it out to be. There’s going to be some serious bumps and bruises along the way.

Here’s how I know…

The Trillion Dollar Wealth Transfer

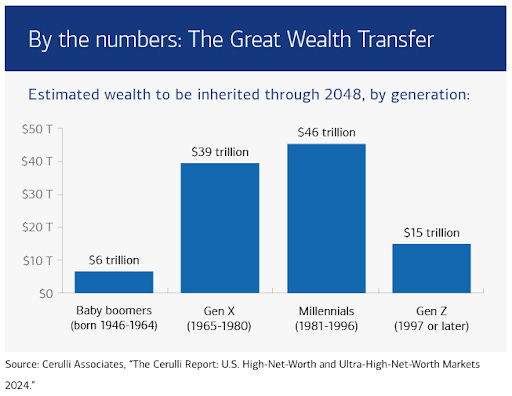

Between now and 2045, trillions of dollars in assets—think retirement accounts, homes, businesses, investment portfolios, trusts, and insurance proceeds—will move from older generations to their heirs, charities, or the government.

There have been multiple attempts at putting an exact number on this tectonic shift. You may have read $70T, $84T, and now $124T by now.

Of those trillions of dollars exchanging hands every year, Cerulli Associates tries to quantify just how much each generation could inherit over the coming decades, with $18T going to charity.

While trillions with T is a big number, much of it is concentrated among a small subset of families. This is our first fork in the road. When you zoom in, the average person isn’t inheriting millions because the average person doesn’t come from an extremely wealthy family. A disproportionate share of this wealth sits with families already in the top 10%, and increasingly, the top 1%. In other words, the wealth transfer isn’t going to be this great democratizer. It’ll likely carry over the inequality we already see and feel.

But concentration aside, the next crossroad is execution.

If you’re like most American families, a house, a few investment accounts, and an IRA are still at play here. It may not be life-changing, quit your job tomorrow, money, but every little bit helps.

The next challenge will be avoiding burdensome taxes on that wealth.

Yes, actual taxes, but also the time spent unwinding and redistributing an estate. Family feuds, court fees, and attorney fees are just the start… if you let it.

As we continue to become an increasingly opulent nation, for some families, passing wealth won’t be as simple as just writing a Will.

It will require extensive planning. Lifetime gifting, layering different types of trusts/entities, stress-testing liquidity needs, preparing for Fed and state-level death taxes, or some combination of each. As the current holder of this wealth, it will be their responsibility to ensure that their heirs are in the best position to receive it.

But this is where your grip on the wheel can get a little tighter.

Even the best intentions can run into forces bigger than all of us: generational differences.

A Generational Divide

According to the U.S. SBA, there are about 35 million small businesses in this country as of 2024-2025.

Still, only ~19% of family businesses transitioned to the next generation in the last five years. The numbers show that most small businesses don’t survive the founder’s exit. Why is that?

The culprit typically falls into one of two camps: a lack of succession planning on the front end and/or a lack of interest on the back end.

I fear my driver, Mark, is dealing with each issue.

Older generations built wealth through the homes they bought for three pennies and lint in their pockets, pensions and retirement accounts linked to some of the great bull markets, and business ownership. But they also value hard work, loyalty, and the pride of building something with their own two hands.

We grew up in a completely different world.

Broadly speaking, the younger generations value flexibility, autonomy, and speed with less hassle. We tend to opt for experiences over material things because material things don’t have sentimental value like they used to. Most tangible items have become cheap, undifferentiated, and hyper-commoditized. But let’s not confuse the word “cheap” with inexpensive, though.

Let’s face it, today’s definition of success is being young, with social capital, and having as much money as possible. And with that as the baseline, it changes how we view risks.

So what kind of effect will this have on markets?

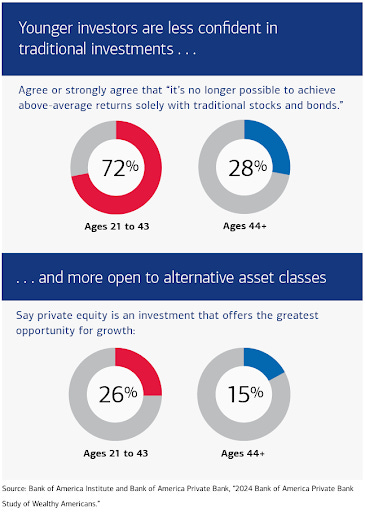

Lauren Sanfilippo, a senior investment strategist at Bank of America, writes, “Younger investors are more open to new financial vehicles, including alternative investments.” As much as we can warn people that private equity and crypto in 401(k)s may not be the right approach for everyone, some people will still need to learn for themselves.

We’ll see investor preferences shift as these dollars migrate from older, more risk-averse households to younger, digital-native households with longer time horizons and a deeper comfort with tech-driven solutions like direct indexing, tax-loss harvesting, and auto-rebalancing.

But one thing is for certain, human behavior won’t change.

Viral manias will create scorching demand, which will create new bubbles. And new market dynamics won’t always act like the old ones. Will have our own vomit-inducing drawdowns and “is this the top?” headlines, but with time on our side, a rising tide should lift all ships.

The Yellow Brick Road

Now, I know nothing about Mark’s son’s background, if he has siblings, or their family dynamic, for that matter. But another detour that can come up for families—especially when leaving intricate yet less liquid assets like homes and businesses—is to simply leave things to their kids equally.

Inheritances don’t have to be “equal” to be fair.

David Handler, a distinguished trust and estate attorney out of Chicago, writes,

“Take a client with a family business in which two of their children were involved and a third was not. Dividing ownership equally among all three children would likely create unnecessary conflict. Instead, the client could leave the business to the two children who were active and provide the third child with different assets of comparable value, such as cash or life insurance. And the amount left to the third child doesn’t necessarily have to equal the value of the business, which will change over time.”

But, as we’ve seen, what if the kids just don’t want the business?

Some owners end up shutting the business down and liquidating whatever’s left.

Others know they have too much tied into it. Whether it be employees or customers, who rely on the business with or without them. They’ll pursue a sale to a private equity aggregator or strategic buyer who can absorb the costs and keep the lights on.

And more often than you think, they/their kids are hopping on sites like BizBuySell.com. They want a clean exit. The kids have zero interest in running payroll, marketing, and vendor relationships for a business they didn’t start. Services like this are all the more evidence that retirees are looking for liquidity and literally any way out.

Although a trillion dollars of wealth being passed down sounds great—especially when the younger generations are desperately trying to find ways to afford an enjoyable life, buy homes, and fund the education of their own children—the road to the trillion wealth transfer isn’t paved with gold.

It’s going to be a little bumpy, filled with detours, and some wrecks so bad you can’t take your eyes off it.

But it doesn’t have to be.

Above all, I think the biggest fallacy is that the headlines make it sound like it’s finite.

Like this generational occurrence will somehow slow down or stop altogether by a certain time. Passing down wealth and values will always be happening under our noses, whether we hear about it or not. It’s the human condition. This is why this will be a conversation that goes on forever.

So get ahead of it.

The best way to get ahead of all this is to talk to your kids. Have family meetings.

Have the hard conversations about why assets are divided a certain way, why a business goes to one child, or why charitable giving is part of the plan. Better now, while you have a voice, than leaving it to vague writing in documents they don’t understand or have the bandwidth to parse through.

If you’re stuck, bring in a professional. You don’t have to do this alone.