“I make good money, but why do I feel like there’s nothing left at the end of the month?”

This is a common statement I hear from people who live in areas with a high cost of living.

These folks typically earn six figures, have solid careers, and still feel like they’re running on the treadmill of life with no financial progress.

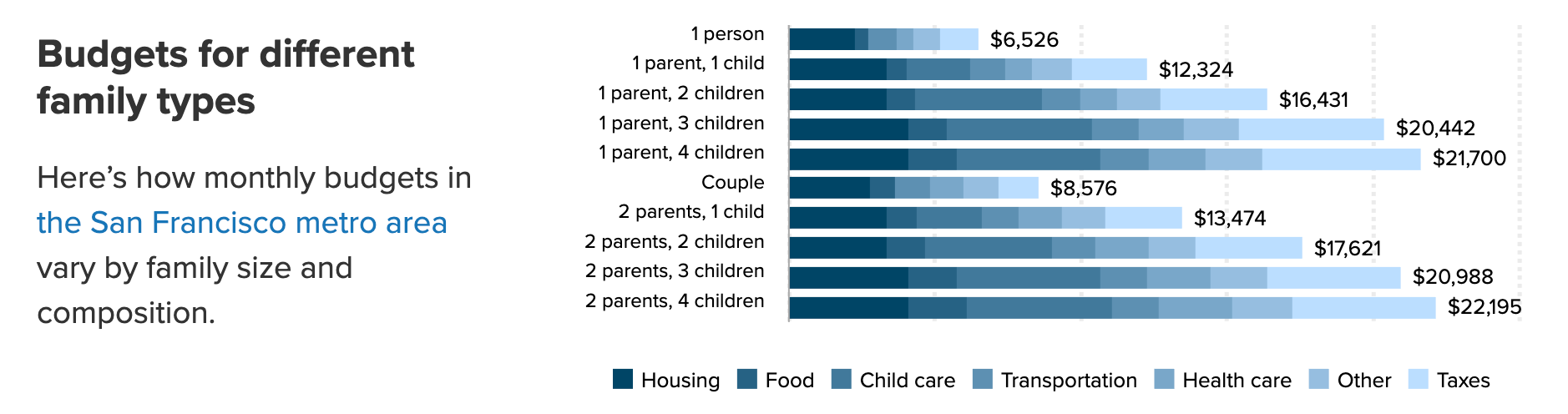

The EPI, a non-profit think tank focused on economic equality for all, has a family budget calculator that shows that the typical monthly budget of a family of four in the New York metro area is $12,784! The Bay Area in California is even higher, coming in at $17,621.

If you can relate, just know, it’s not just you. We’re all feeling it.

Being rich and feeling rich are two very different things. Members of the Gen Z generation say you need $1.7 million to be wealthy. Millennials and Gen Xers say $2.1 million. Baby Boomers report $2.8 million. Regardless, on average, this is a 21% increase from 2021.

The point is: feeling “wealthy” or “rich” is a moving goalpost.

This may never change.

Over the last three years, we’ve experienced higher inflation than in the decade preceding it. And while I’ll always defend Jay Powell and the extraordinary work he’s done in his tenure, it’s hard to ignore the toll higher interest rates on high-ticket items have had on the recent economy.

The national average car payment is now $745 for new cars and $521 for used vehicles. And even with the carrot of an interest deduction on auto loans dangled, most won’t benefit from the OBBA provision offering up to a $10,000 deduction on U.S.-made cars. According to Caribou, “only 2.8 million Americans—less than 3% of the 100 million with auto loans, will qualify for the deduction.”

Home prices and mortgage payments? Up nearly 50% since 2017.

In July 2017, the median home price in New Jersey was listed at $330,601. Today, it’s closer to $569,314.

Assuming you put down the same 20% to avoid PMI:

2017 mortgage: $1,429/month

2025 mortgage: $2,966/month

And this is all before everything else it takes just to stay afloat in this country.

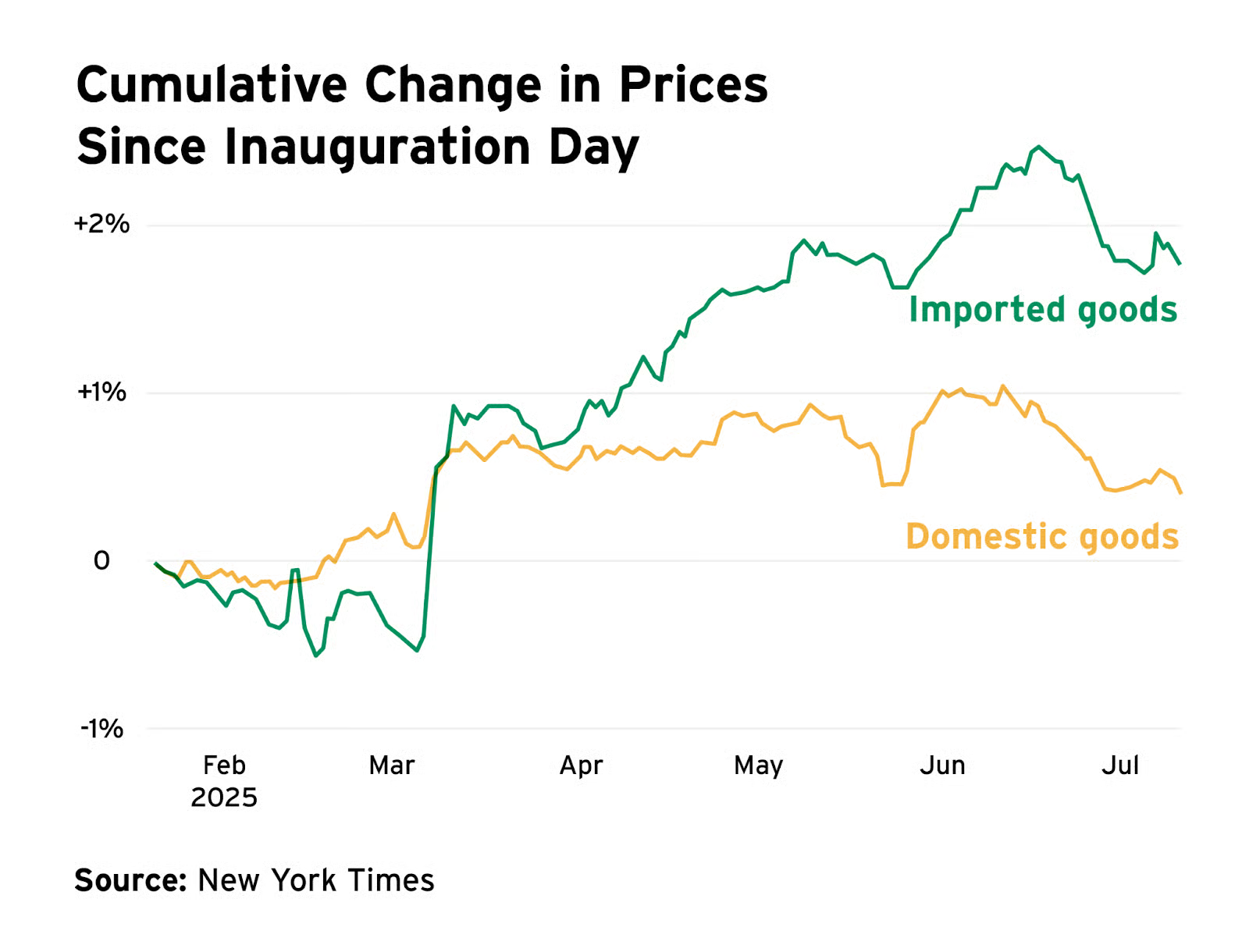

And now, it’s evident that tariffs are slowly trickling into our normal lives. Despite PPI staying unchanged month-over-month, we see that the price of imported goods has eclipsed U.S.-made products.

Prof G Markets, CPI vs. PPI: The Crucial Inflation Detail Everyone’s Missing

And my colleague Callie writes, “According to these daily receipts, tariff collections have jumped from $9 billion to $28 billion per month this year, boosting the effective tariff rate to around 10% – near the highest in a century.”

This may be good in terms of tax receipts—especially considering the corporate tax rate is permanently set at 21% by the OBBA—but not for you and me. Let’s not kid ourselves, higher prices are sticky, and somebody will have to foot the bill.

And it’s typically not corporate America.

Net Zero

When I talk to families who feel this way, I call it operating at “Net 0.”

Net zero means that after all your expenses and savings, you have nearly nothing left over in your checking account.

There are really only two ways to reach net zero:

By choice—You automate savings and investing first, then spend what’s left. Your goal is to make sure every dollar has a purpose.

By force—You get to the end of the month, and everything’s gone. You may not even know where it went, but you know it’s not there, even if it doesn’t feel like frivolous spending. It just disappears.

So what’s going on?

What could be the issue?

I’m not here to spend-shame anyone. But here are the usual suspects:

1. The need to have everything.

We’re living the American Dream! As I mentioned in that post, we’re navigating a world where we can do almost anything or have it delivered to our doorstep—convenience has never been more accessible. But with that accessibility comes expectation from others.

Kids’ sports and activities.

The car (Guilty!)

The house in the best neighborhood.

We convince ourselves that these are baseline needs. But even among those doing well, it still doesn’t feel like enough.

In other words, the middle-class don’t feel rich—not because they aren’t doing well, but because the pressure to keep up (or keep spending) never stops. And when you live in the big metro areas, it’s constantly in your face.

As Nick Maggiulli put it:

“The upper middle class are learning this the hard way. They are finding out that the exclusive wealth they thought they had isn’t so exclusive after all. What was once a marker of distinction has become a victim of popularity.”

Maggulli’s post highlights that being Level 3 rich just isn’t that uncommon anymore. And retailers know this. That’s why they don’t have to lower prices to get more sales. They know you’ll spend the money anyway.

My takeaway: adopt the mantra, “all that I have is all that I need.”

2. Budgeting

I know the term “budgeting” makes people want to throw up—but a lack of oversight over spending is a major issue.

Tools like Rocket Money, YNAB, or even just a simple spreadsheet can help. The idea isn’t to nickel-and-dime yourself, it’s to know what’s going where.

Once you can identify what’s left over and even areas you could be more efficient, you can sneak in ways to automate your investing. Even if it’s only small amounts. For me, if that money is not redirected, it will find a way to get spent. This is why I also strive for net zero, but I don’t feel guilty for spending on what I want because I know my monthly savings target has been hit. In theory, it will only go up from here as my income increases.

3. No plan

Even if you’re a disciplined saver, without a financial plan, there’s no way to track progress. You’re just saving… and spending the rest. Net 0 by choice, with no purpose.

A real financial plan gives you:

A clear view of your assets and income

Defined goals and priorities

A roadmap to get there

Proper asset allocation to match those goals

Progress tracking along the way

Whether you know it or not,

If this is you, you’re not alone.

Reducing costs isn’t just hard—it might require downgrading your lifestyle, and trust me, no one wants to do that.

You work hard, and I’m a big believer that you deserve to have something that reflects that hard work does eventually pay off.

Everyone says not to buy the new car—because it’s a status symbol, it depreciates fast, and it slows your path to building wealth. And they’re not wrong. But if you can afford it, understand the tradeoffs, and it genuinely brings you joy… why not? Money is a tool. And sometimes, that tool is best used to improve your quality of life—not just your net worth.

But once you get past the tangible things, if you want to start making real progress, you need a few things:

A spending plan and finding any areas where you can automate saving and investing to get you to net zero the right way. A financial plan to know where you were, where you are, and where you’re going. And realize that someone looks up to you. Whether you know it or not, plenty of people wish they were in your position. You should take pride in that.

Finally, do something in your life that fills your cup outside of money. Do something that makes you feel complete.

Maybe that means you reduce your commitments. Josh Brown wrote No More Side Quests. He wrote it in 2021 and it still hasn’t left my brain. Similarly, Blair wrote a great post titled “The Superpower of Saying No.” Make sure you check these out.

Whatever it is, do it for you.

If this all resonates with you, it might be time to work with a professional.