The American Dream Is Not Dead: You Have to Ask, Whose Dream Is It?

A few years ago, my brother decided to uproot his life and move to Asia.

He started teaching English as a second language to students around the world and came to the realization that it was less expensive and made the time zone differences easier to manage. Not to mention more exciting than staying in Georgia. Now, bouncing between Vietnam and Thailand, chasing a version of freedom that didn’t come with a 401(k) or health insurance.

It came with something else: autonomy, making the world a smaller place, and life at a slower pace.

I took the complete opposite path.

I chose the more traditional route—got a job in NYC, chasing financial freedom, and dedicated myself to building a future where my children (his nieces and nephews) won’t have to live the life my brother and I did growing up. For me, the financial industry and writing have become a ticket out.

Two people from the same place. Two completely different paths.

We’re both chasing different versions of the same thing: the new American Dream.

We all know the old version.

The white picket fence. The large suburban home. The luxury car. The big-screen TVs glowing in multiple rooms. The safe, reasonable nine-to-five. The corner office.

Yeah, we threw that script out the window.

Why? Where did that really get us?

Student loan debt that will outlive most of us. A housing market few can afford to enter. A political system that can’t agree whether our country is headed in the right direction or not, while simultaneously hellbent on driving up the federal deficit.

Are we just f*cked?

I don’t think so…

The fantasy of the American Dream didn’t die. It grew up. It expanded. It stopped being one-size-fits-all. Today, it’s about financial freedom and autonomy. And for many of us—especially my generation—that dream only feels achievable through technology, creativity, and influence.

Which brings me to my generation: Gen Z.

Gen Z’s Nightmare

Each generation has lived its own version of the American Dream.

Some ‘made it’ and left them wondering, Isn’t there more to life? And then there’s a growing group who look at all of it—the house, the job, the debt—and think, why would I spend my life chasing someone else’s dream, just to end up burned out and barely getting by?

The Silent Generation and Boomers largely achieved it. They bought homes at affordable prices, enjoyed pensions, and experienced steady wage growth. Many were in their 20s between the 1940s and 1970s—what my colleague Nick Maggiulli describes as one of the greatest times for homeownership.

Of Dollars And Data: Has the American Dream Become Unattainable?

Gen X had a more mixed reality. Some thrived. Others struggled through multiple recessions. Many are now heading into retirement wondering if they saved enough to get them through to the other side.

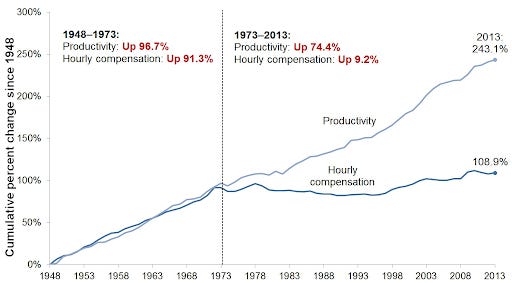

They were told to keep their heads down, grind, and success would follow. But the numbers tell a different story. According to the Economic Policy Institute:

“Starting in the late 1970s, policymakers began dismantling all the policy bulwarks helping to ensure that typical workers’ wages grew with productivity… From 1979 to 2020, net productivity rose 61.8%, while the hourly pay of typical workers grew far slower—increasing only 17.5% over four decades (after adjusting for inflation).”

We’ve watched the effects of those policies play out for decades, yet the message remains the same: work harder.

Sure, technology and innovation have made work more efficient and increased total output. AI is slowly becoming an integral part of my job, and I’m sure it’s not just in my industry. But what about wages? They’ve flatlined. Meanwhile, the cost of education, housing, and childcare has skyrocketed.

Millennials arguably got hit the hardest. Many entered the workforce during the Great Financial Crisis. They’re now burdened with student loans, flat wages, and a housing market that had already begun to slip out of reach. To no fault of their own, many relied on their parents just to get by.

And then there’s us—Gen Z—the first generation to grow up fully aware that the rules of the game have changed.

Despite being the most educated generation, we’re also one of the most financially strained. Megan Carnegie at the BBC notes that:

“At Gen Z’s age, older people worked 40 hours a week and made enough money to buy a house and have barbecues on the weekend,” says Corey Seemiller, an educator and TEDx speaker on Gen Z. “Gen Z works 50 hours a week at their jobs, and another 20 hours a week side hustling, yet still make barely enough to cover rent.”

Ask someone my age and they’ll tell you this: hard work doesn’t guarantee better pay. That promise has broken down.

The reality is, 74% of Gen Z workers say they would leave a job due to low pay. And when it takes an estimated $138,000 a year just to live comfortably as a single person in NYC, who can blame us?

This is likely why we have the stigma of being lazy. But the reason for this mindset could be that we see generations before us breaking their backs for years, only to scrape by. Combine that with the cost of the basic wishes of life—education, a starter home, or raising a child—rising much faster than our wage trajectory could ever reach.

We’re not lazy, we’re paralyzed by fear.

We’re navigating a world where we can get whatever we want delivered to our door (thank you, Jeff Bezos and Tony Xu)—but real financial freedom feels farther away than ever.

I feel that a lot of the vision has to do with messaging. Influencers are flying to Mykonos while others are working two jobs and still live with their parents. Both are living out different versions of what it means to “make it.” Knowing this, how could you not want it all today?

And that’s exactly why we’ve started building a new path entirely.

The New Path to Success: Wealth & Influence

Many of us truly believe a 9-to-5 paycheck just won’t cut it.

Saving (alone) just isn’t enough.

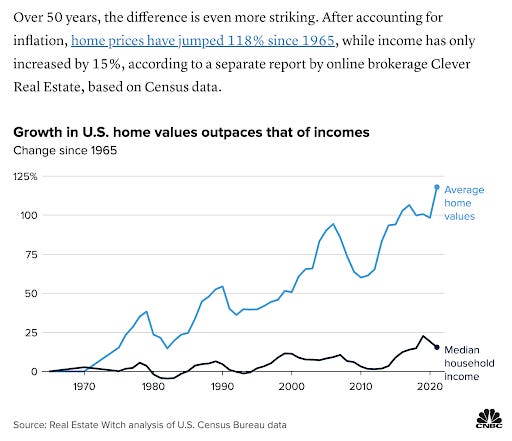

The new American Dream isn’t about owning a house with a white picket fence. We can’t afford the fence.

Homeownership—a cornerstone of middle-class affluence and a catalyst for building wealth in this country—is out of reach for many of us. And it’s not just about the flex of having a house; the lack of opportunity here has major implications down the road. As Steven Bartlett of The Diary of a CEO put it:

“Your house is an asset you can pass down, borrow against, or sell—but you don’t get those opportunities if you’re priced out.”

So what do we do?

We have to take risks.

Because if we don’t, we’re left behind in a system that wasn’t built for us.

Some of those risks look like starting a social media page to share your voice/talents with the world. Others throw money into meme stocks or crypto, chasing the kind of upside most stable jobs rarely offer. Think back to the 2021 GameStop, Robinhood saga. Some of us are scrapping college, opting out of marriage entirely, jobs, or even the country itself.

As MoneyWise puts it, “the new American dream is to leave.”

A growing number of Americans are choosing to start over abroad—seeking out quiet European towns or beachside villages in Asia where health care isn’t a luxury and food doesn’t feel like poison. My brother made that leap. Only returning to the States in short stints. And honestly, I get it.

But no matter where we are, the new marker of success is the same: attention and influence.

Platforms like YouTube, TikTok, Instagram, and Twitch give everyday people a shot at financial independence. Social media is a wide-open lottery ticket.

If the “Hawk Tuah” girl can do it, so can I… right?

A side hustle can become your main gig. And if you play it right, it becomes a full-blown business.

This shift isn’t just touching entrepreneurs—it’s reshaping politics.

Politicians today aren’t just public servants. They’re influencers. Campaigns are brands. Visibility and engagement matter just as much as policy. Like creators, they harness social media, ride viral moments, and monetize attention.

Ed Elson said it best:

“America has fallen out of love with brands and in love with people. People are the new brands.”

And that’s what this new American Dream is about—building a brand, earning influence, and monetizing both.

There’s one caveat I will add, though. My generation tends to have a flair for the dramatics. Despite all these statistics not being in our favor, only time will tell how this all plays out. The wealth in the hands of the older generations will have to be passed down at some point. Today’s 20-somethings will be the next legislators and employers.

Only time will tell whether the decisions we make today are the right ones or not, or whether they even mattered or not.

Choose Your Own Adventure

The dream used to be simple: get married, pop out a few kids, buy a house, work hard for 40 years, and retire comfortably.

But that doesn’t have to be your dream.

You can choose your own adventure.

Want to be a digital nomad? Try it. Don’t be afraid to leave a job (ok… be a little afraid. Have a plan) that doesn’t serve you—emotionally, financially, or spiritually.

The traditional route isn’t the only—or even the best—path to success. The rise of the creator economy proves that you can carve your own lane with relatively low barriers to entry.

And beyond that, more of us simply want autonomy. If we’re going to be glued to a screen until we’re 90, we should at least get to choose what we’re building, who we’re working with, and how we’re spending our energy.

The new American Dream is about doing work that feels good and does good. Building a life we don’t feel the need to escape from.

My American Dream looks like escaping the paycheck-to-paycheck cycle, being a master of my own time, and building a life where I’m not just getting high to get by. A house with a backyard that I can mow on the weekends and toss a ball with my dog(s). Or toss the football or play basketball with my kids. Enough space to store a grill and pull it out in the summer to cook a good steak and char some corn on the cob. Sitting at the dinner table with my kids, helping them with homework that actually stimulates their little brains.

These are my dreams. Your dream may be different.

It’s on you to go get it.