"A small debt produces a debtor; a large one, an enemy."

How to get out of credit card debt

One of my best friends recently reached out to me to catch up, shoot the shit, but more importantly, bust the news that he’s getting married this year!

I couldn’t be happier for him, as he’s been one of my closest friends since high school. We went to college in two different states, and now live halfway across the country from each other. We’re both in the dog days of our lives. Building our careers, trying to see what sticks, and now he’s building a family. So being able to just sit and talk is a rarity these days. So when we did get a chance to talk, we had so much to catch each other up on.

Along the conversation, he was finally able to get something off his chest that he’d been keeping in for months. A topic that effects nearly everyone at some point:

Credit card debt.

He walked me through how he got there, and that before the wedding, this needs to go away ASAP.

You see, on paper, my friend is doing all the right things.

A year after college, he bought a duplex with another friend. They each took a bedroom upstairs and rented out the lower half of the house. They both have good jobs that cover their share of the mortgage pretty easily. But the house wasn’t in game-time shape when they bought it so some cash for renovations went out. The walls needed a paint job. Carpet torn out and replaced with vinyl hardwood flooring. And decent furniture, as they’re renting it pre-furnished.

It was supposed to be the first steps toward building real money.

However, as time went on, he still found himself in a hole.

Ok… let me rephrase that. If you’re caught up on Season 3 of Euphoria, I’m not talking about a full blown Nate and Cassie situation, but clearly something needed to be done.

So how does the buildup start?

I’ll tell you how it starts. It starts with one or two, or like four unexpected costs come up. Your car gets towed because of the worst snowstorm the east coast had in years (twice), you switched to an HSA and doctor visits now come out of your pocket. You rescue a kitten, and now that “free” cat turned out to be the world’s most expensive cat. I don’t know, I’m just spitballing here.

Maybe your HVAC system blows up just as it starts getting nice outside. All work and no play is a recipe for disaster, so you treat yourself to a nice vacation overseas. Concert tickets. Pick your poison.

But that’s not what does you in.

It’s when normal life continues around it.

Gas to get back and forth from work. Food for the week. Date nights. Rent and all the other household bills.

It doesn’t replace the spending that you would normally do. It piles on top of it. And when it’s put on your credit card, those numbers start to stack up.

To my surprise, I found that food prices in this country have increased more than 34% since pre-covid. Sure, that’s been behind us for 7 years now. Yet more recently, food at home, or grocery prices, rose as much as 11.8 percent in 2022 alone! According to the USDA, food prices were 2.7% higher in March than the same period last year, and increased another 3.2% YoY for April.

But that’s just food, an expense we largely can’t get around—whether on credit or not. And don’t even get me started on gas prices.

Actually, I will get started. We’re starting to see and feel the effects of this war dragging on. We got confirmation that last month, the average consumer’s disposable income lagged consumer spending. Which is a fancy way of saying, on average, we’re spending more than we’re making. So when you’re already financial living on the edge, and non-discretionary costs keep rising, you may have no choice but to get by by borrowing from your future self.

To add to that, Axios makes a good point that despite sentiment, what we’re feeling on the ground, consumer spending continues to hold strong. Which is likely why haven’t seen the market really react at all to the latest CPI and PPI reports the way I would have expected. However, “aggregate spending is still being supported by the wealth effect and the upper end of the K-shaped economy, but that support is doing more of the heavy lifting—making the overall spending backdrop look increasingly uneven and fragile,” Fitch Ratings’ head of U.S. economics writes.

Going into credit card debt doesn’t necessarily mean you’re bad with money or that you’re fiscally irresponsible.

It comes for us all at some point.

The average cardholder holds a balance somewhere between $6,500–$6,800. And for households earning over $100,000, it’s often closer to $7,000 or more. Unless we’re in some sort of economic contraction, as a nation, it feels like we’re consistently hitting a new record in credit card debt.

Again, going into credit card debt doesn’t mean you’re bad with money. But it does mean that a pivot needs to be made before this manageable problem becomes a much bigger problem.

The last point I’ll make before explaining to what do about it is: the problem with high-interest debt is that it’s regressive in two ways.

The first way is that it pulls money for the future into the past.

You’re paying for things you already consumed instead of putting that money toward things that will help you get ahead—building a solid emergency fund to avoid these problems in the first place and investing to pay for the things you want to spend on in the distant future.

“A small debt produces a debtor; a large one, an enemy.”

Second is what it does to your mental state. My friend sees himself as a provider and a hard worker, so if he just put his head down, he should be able to tough it out. Yet this weight sat on his mind for a long time before he even shared with anyone, let alone his future wife. That’s not a knock on his communication skills; these conversations are simply not that easy. High interest debt can build up fast, but take much longer to fully pay off. It can feel like your not making progress even when you are. That kind of pressure on yourself can eventually make you your own worst enemy.

With all that said, what do you do to get this monkey off your back and move on with your life?

If you have the cash flow and a decent savings already built up, that’s great.

I wouldn’t recommend you completely wipe out your savings just to close out your outstanding balance(s). While it might feel great in the short-term, if it’s not what got you there in the first place, living on the edge will certainly bring you back to where you were—like a dog chasing his own tail.

Your emergency bucket is there to act as a cushion for the expected-but-untimely, and unexpected expenses that come up.

At the onset, there are two ways I like to go about it:

If it’s spread across a couple of credit cards, start with the lowest balance first.

This is going to help you feel like you’re making progress. Pay it off it in full and keep reading for what you’ll do next.

Consolidate the balances.

This is not a debt consolidation loan. You’re simply pulling the balance from one card and combining it with another. And before you spaz out on me and say what about the interest on this one large balance, stay with me.Check your credit card app/website to see if you have access to 0% APR on balance transfers.

A 0% balance transfer allows you to essentially wipe out the total interest you would have paid on the transfer. But you do need to pay off most, if not all, of your transferred balance during the 0% term for this strategy to work. This has worked for me and every since then, I swear by it. Be aware, this strategy isn’t “free”—there’s typically an upfront transfer charge to do so. The price of admission.

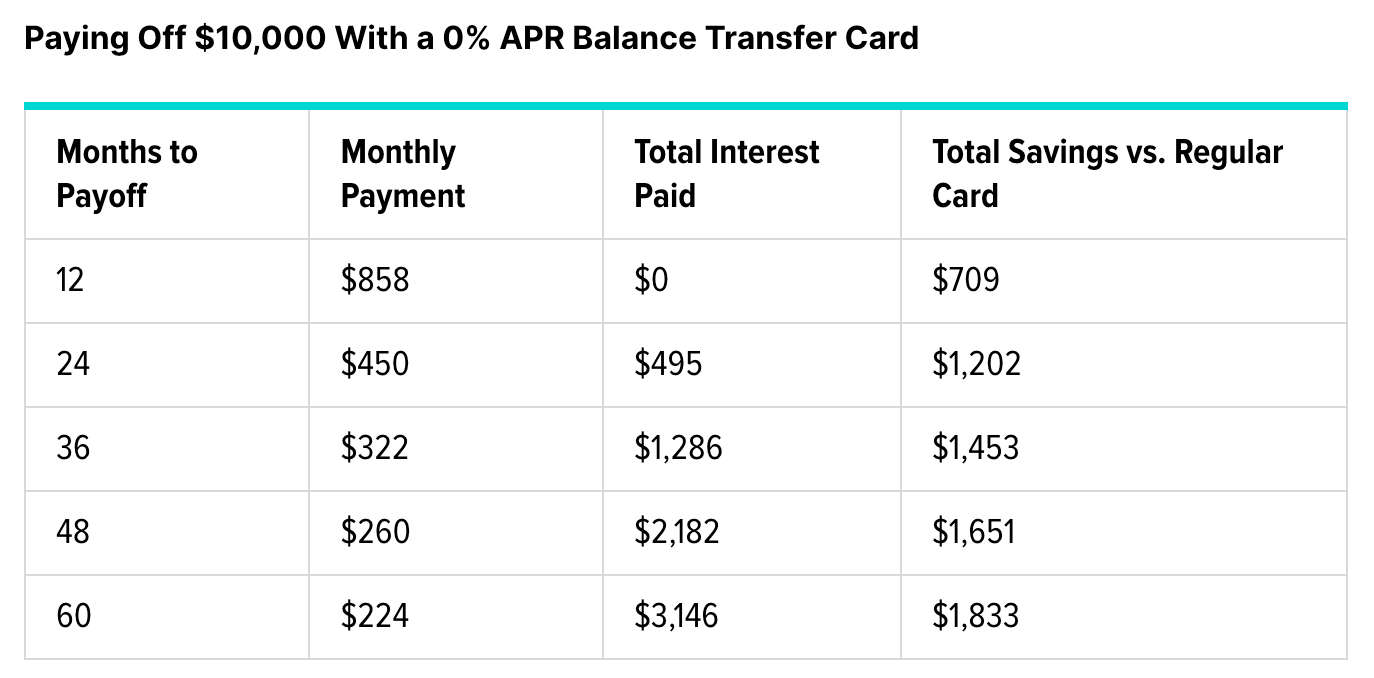

To pay off $10,000 in credit card debt within 36 months, you will need to pay $362 per month, assuming an APR of 18%. You would incur $3,039 in interest charges during that time, but you could avoid much of this extra cost and pay off your debt faster by using a 0% APR balance transfer credit card.

Obviously paying it off in full is ideal, but what if that’s not possible?

With your next paycheck, here’s what you’re going to do…

If you’re really tight on cashflow, it’s ok to reduce your retirement savings for a short while.

While this advice might be controversial, to me, it’s better than telling you to drastically cut your spending and reprioritize your life. (1) you know changes need to be made, and (2) you probably didn’t wish for everything to be so expensive. That’s just the way things are.

This means you temporarily pull back on 401k/IRA contributions to stabilize cash flow. Which is fine for a short amount of time. But understand the cost. One or two months is a decision. Five or six months is a trend. And trends tend to have inertia. If you wait too long, your new paycheck will become your new standard of living, and that defeats the purpose/point of what we’re ultimately trying to do here: get out of debt and back on track to securing your financial future.

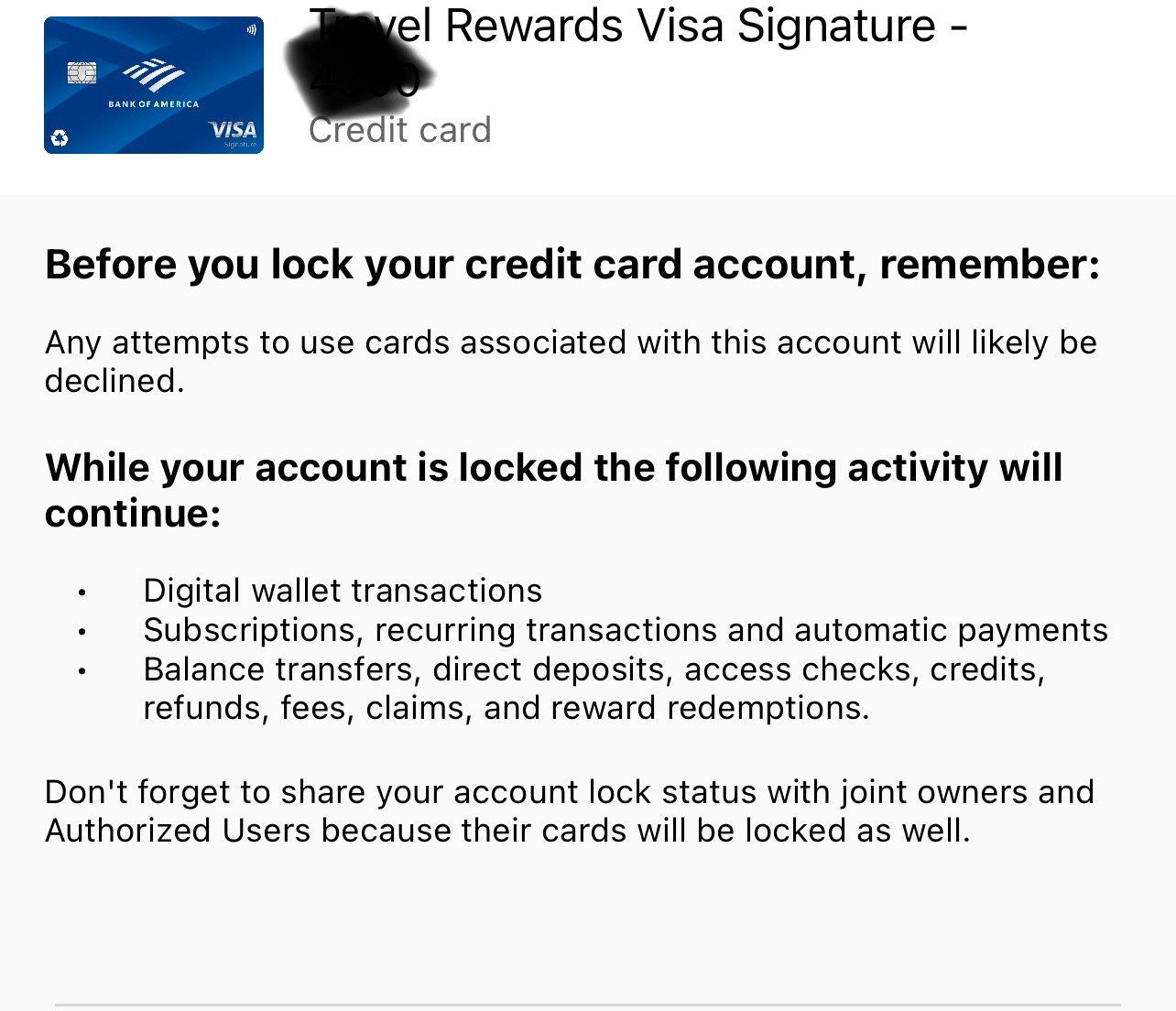

Next, take your card out of your wallet - let air out for a while.

I do that mean literally and figuratively.

If you don’t actually want take it out of wallet: lock your card.

This a no harm, no foul way to put yourself on ice and really be cognizant of what you’re spending money on. “Normal life”—things like subscriptions and billpay—will resume in the background, but your card will get declined if you physically (or Apple Pay) try to use it out in the wild. This abrupt cue should make you assess whether this transaction is really worth it, and if so, to just use cash.

Finally, reassess your spending and optimize the things you’re already going to spend on.

If travel is important to you—and for a lot of people it is—learn how to do it more efficiently.

There’s a right way and a lazy way to spend on experiences. Same outcome, but very different cost. Look into travel-hack content that gives you legit and actionable advice how on where and how to save on your next trip. Not just affiliate links that helps them more than it helps you.

If you’ve already pinpointed your next destination, I guarantee you some influencer has already been there. Don’t try to reinvent the wheel. Look into their itinerary. Where and with who they booked their stay, and if it’s still out of our price range, MOVE ON.

To that end, find a card with benefits that actually benefit you. It does you no good to pay $600 a year for an AMEX card just for the flex. I’ve said before, I prefer cash back programs—it’s like I’m getting a 2-6% discount on what I was already going to spend on—but I’ve seen many people make the most out of points. Do what makes the most sense for your situation.

That’s all for me.

Until next time.

What is credit card debt?

Just use it and pay it off each month?

"Going into credit card debt doesn’t necessarily mean you’re bad with money or that you’re fiscally irresponsible."

---

I would have to disagree. If you have to use a CC to cover an expense and you can't pay it off at the end of the month, then you haven't put aside enough money for all the emergencies that pop-up.

Also, having savings when you are paying monthly interest on CC debt is foolish. Paying 15-30% interest to the the CC company while your savings earn 3-4% (if you are lucky) is nonsensical. Use the savings to pay off the CC debt and then stop using the CC unless you can pay the amount off each month.

I use CC's extensively for the rewards and haven't paid CC interest in decades.